Business As Usual For Investors In 2022

It’s no secret there has been significant media commentary surrounding the recent interest rate rises leaving many mortgage holders thinking about the need to tighten their personal budget to ensure they are able to manage their cash flow. However, it is important to note that the impacts felt by owner occupiers who hold a mortgage are not entirely the same as the investor.

Why Is This Happening?

One of the jobs of the Reserve Bank of Australia (RBA) is to control inflation. This is extremely important for the long-term economic health of the country. The way the RBA do this is by managing the cash rate. Put very simply, by increasing the cash rate the cost of living is increased and consumer spending is decreased. This is what helps to control inflation.

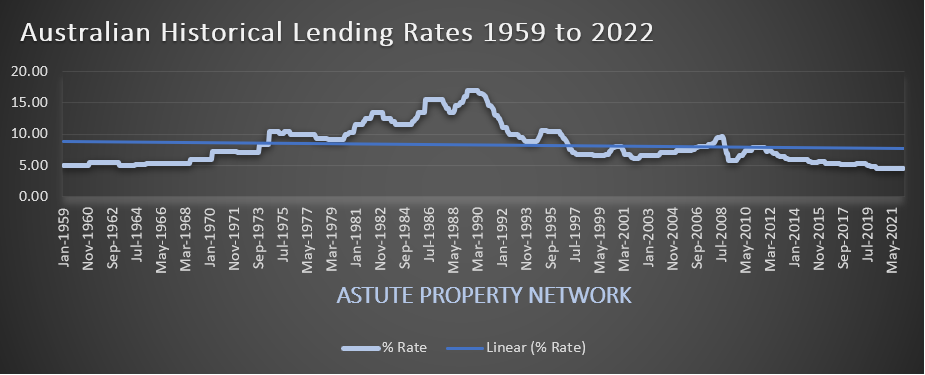

A Brief History On Mortgage Rates

If the cash rate increases the organisations that lend money will pass that increase onto consumers. This is fantastic for your local news, a current affair, and media outlets as they finally get to drum up some doom and gloom. Leading some people questioning if now the right time to invest in the property market.

We have seen this many times before and although there is no reason to believe we will be subject to the rates of the 80s and 90s, it’s important to remember that we have enjoyed record low rates for a very long time.

In 2002 the average mortgage rate was 6.57% compared to 4.52% in April 2022. The average variable mortgage rate in Australia over the past 63 years has been just 8.22%.

Below is the history of interest rates in Australia since 1992 showing the average rate has been 6.93% over the past 30 years.

Should I Invest?

Investors have continued to make high returns on real estate over the past 63 years and there is every indication that property will remain an effective investment strategy well into the future.

Interest rates are unlikely to drop again for quite some time now, however it is equally unlikely that they will increase at an aggressive unmanageable rate. Australia is a long way off being able to say we have recovered from the economic impacts of COVID-19, recent floods, droughts and fires. Therefore, it is not a question for investors of if or when they invest it is a question of where and how they invest.

So, in essence the questions have not changed for investors serious about making their hard earned money work for them. The key question for any property investment strategy is; where can I get the best returns and how much can I invest to ensure a sustainable cash flow.

What Can We Do As Investors To Help Mitigate Any Potential Future Risks?

Location & Property Type

Do your homework before you invest to ensure that you are investing in an area that will continue to be in high demand but further to this, make sure the dwelling type you are looking to purchase in this location has a proven track record for growth. There is a well-documented and acknowledged housing shortage in this country however not all suburbs and property types are going to see equal growth. Research remains the key to savvy property investing in Australia.

Purchase PriceComplete a realistic cash flow analysis of the property with a realistic future interest rate to see what your parameters are. This is not as simple as your mortgage repayments vs your rental yields. You should include insurances, management fees, council rates, maintenance and any other foreseeable costs. Don’t forget to include any tax benefits that you are eligible for such as depreciation.

If you don’t know how to forecast the cash flow estimates, employ the services of people who can.

Rental YieldThe housing shortage and restrictions on new builds due to shortages in material as well as labour has meant that there will be significant pressure placed on the rental market over the coming years. This is good news for investors as supply weakens and demand increases there is definitely scope to adjust rent.

Conclusion

While it is true that some areas in the country are showing signs of slowing such as parts of Sydney and Melbourne, the vast majority of the Australian property market is still producing positive figures and is remaining buoyant.

There is a well-established property cycle in Australia and each region of the country experiences the cycle at different stages. Understanding how to identify the regions that are experiencing their growth stage puts you in a better position to capture strong returns in the first several years before the region slows which is cyclically what it is designed to do.

If history is any indication of the future (which it usually is), the Australian property market will continue to deliver sound returns both in capital growth and rental yields, however not all cities and regions will perform the same.

Just like any decade in history the winners will be those who approached investing like a business and took time to understand and educate themselves instead of being influenced by doom and gloom in the media. Or furthermore, sought professional guidance when they needed to.

"I think people often forget that while the cost of some things obviously go up in an inflationary environment I.e. mortgages, fuel, cost of living; being an investor gives the benefit of income returns also going up like rents, interest on term deposits etc. In many ways an inflationary environment can be viewed as a zero sum game for smart investors” Alex Minter – Director Astute Property Network

Source – Graph data Reserve Bank of Australia Disclaimer: The views of the author, either expressed or implied, may not represent the views of Astute Property Network Pty Ltd. Every effort is made to ensure the accuracy of the information contained within this document. The information is not intended as financial advice and does not take into account your personal financial position or needs. You should always consult your financial specialist before making any changes to your finances.